Last spring, I lost three homes in a row.

Not because my offers were low. Not because I had bad credit. I lost them because I kept submitting static offers in a market that was moving faster than I could react. By the time I revised my bid, someone else had already signed the contract.

After the third loss, my real estate agent sat me down and said something that changed everything: “Stop guessing. Let the clause do the work.”

She was talking about an escalation clause — a provision I had vaguely heard of but never fully understood. A month later, I used it to win a bidding war on a home I genuinely thought was out of reach. The final purchase price? Exactly $7,000 more than I would have offered on my own. But I got the house, and I didn’t blow my budget.

Here’s exactly how I structured it, what I learned, and what I wish I had known before losing those first three homes.

What an Escalation Clause Actually Is (In Plain Language)

An escalation clause is a provision you add to your purchase offer that automatically increases your bid by a set amount above any competing offer — up to a maximum price you set in advance.

Think of it as your personal bidding assistant. Instead of sitting by the phone waiting for counter-offers, the clause handles the competition for you within the boundaries you define.

It has three core components:

Your base offer. This is the starting price you submit — not your highest number, but a fair and reasonable opening bid that reflects what you think the home is worth.

The escalation increment. This is how much your offer will beat a competing bid by. Common increments are $2,000, $5,000, or $10,000 depending on the market and the price point of the home.

The price cap. This is the ceiling — the absolute maximum you are willing to pay, no matter what. The clause will never push your offer above this number.

It sounds simple because it is. The complexity is not in understanding it. The complexity is in setting those three numbers correctly.

The House I Was Trying to Buy

The home was listed at $485,000 in a suburb where anything under $500,000 was getting five or more offers on the first weekend. It was a four-bedroom with a finished basement, freshly updated kitchen, and a corner lot. I had been watching that neighborhood for months.

My agent called me on a Thursday evening. Offers were due by Sunday at 5 PM. She already knew from the listing agent that multiple buyers were interested and that the seller was expecting strong numbers.

I had pre-approval for up to $540,000, but I was comfortable spending no more than $520,000. That ceiling mattered to me, and I stuck to it.

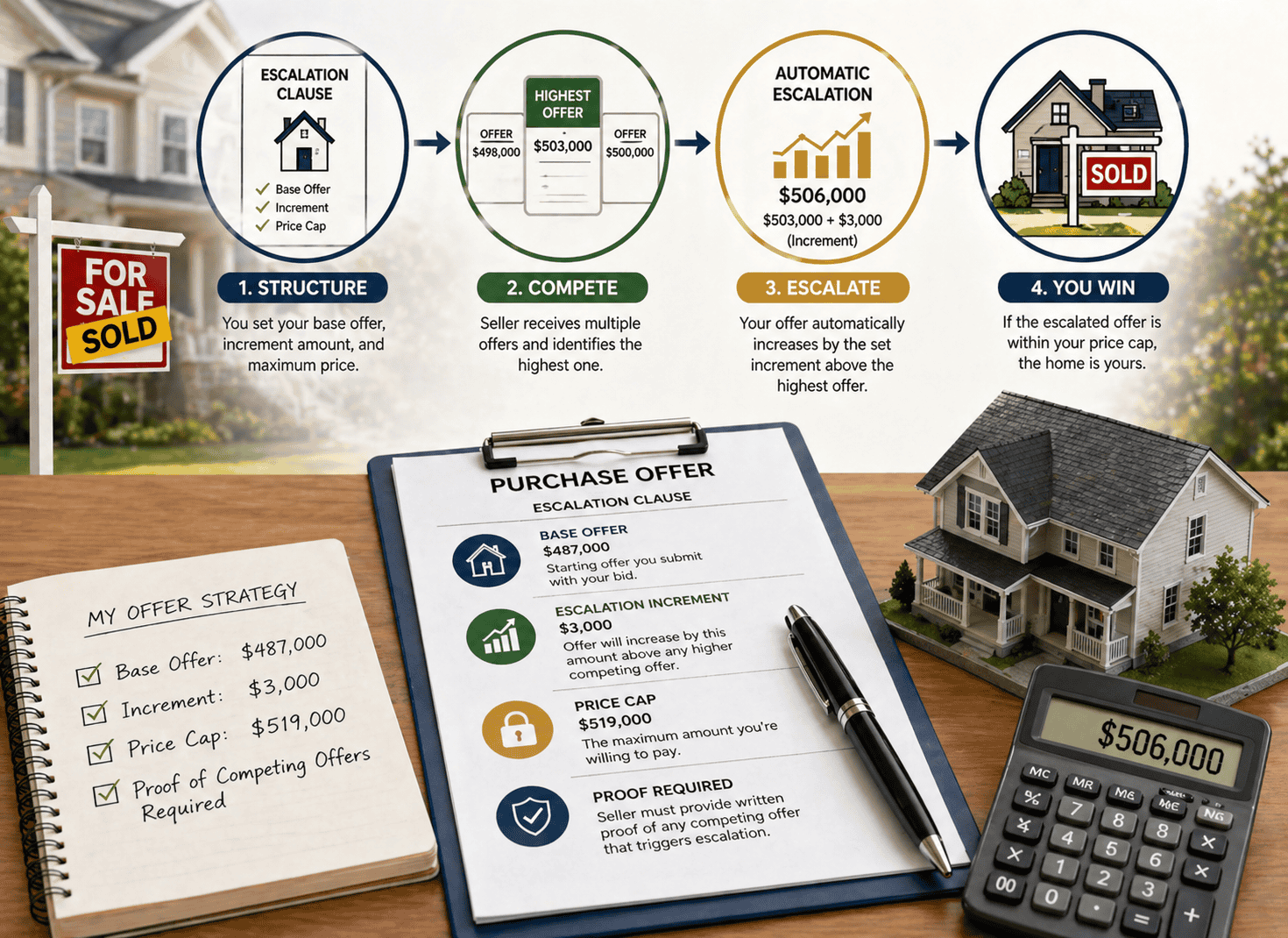

How I Structured My Escalation Clause

After a long conversation with my agent, we landed on this structure:

- Base offer: $487,000 (slightly above list, showing I was serious from the start)

- Escalation increment: $3,000 above the highest competing offer, net of seller concessions

- Price cap: $519,000

We also added a clause requiring the seller to provide written proof of any competing offer that triggered the escalation. This is a critical protection. Without it, a seller could theoretically inflate numbers to push your price up. With it, you keep the process honest.

Why $3,000 and not $5,000? My agent made a point I have never forgotten. She said that in a competitive seller’s market, you want your increment to be meaningful without being reckless. A $1,000 increment looks cheap. A $10,000 increment can signal desperation and push your final number higher than necessary. Three thousand felt like the right balance for the price point.

Why $487,000 as a base instead of $485,000? Because starting above list price signals seriousness to the seller without needing the clause to do all the heavy lifting from the first dollar.

What Happened When Offers Were Reviewed

Sunday night, my agent got a call.

There were four offers. The highest competing bid before escalation was $503,000. Because of my clause, my offer automatically escalated to $506,000 — $3,000 above that number, well under my cap.

The seller accepted.

I paid $506,000 for a home listed at $485,000. Was it more than the asking price? Yes. But it was $13,000 less than my maximum, and I walked away with the home I wanted without having to guess, panic, or go back and forth with counter-offers.

That is the real value of an escalation clause. It is not just a bidding tool. It is a clarity tool. It forces you to know your limits before emotions take over.

The Mistakes I See Buyers Make With Escalation Clauses

Since then, I have watched friends and family attempt this strategy with mixed results. Here is where things tend to go wrong.

Setting the cap too high. Your cap should reflect what the home is genuinely worth to you — not just the absolute ceiling of your pre-approval. If your clause escalates to $540,000 but the home appraises at $510,000, you will need to cover that $30,000 appraisal gap in cash or renegotiate. Always think about the appraised value, not just the financed amount.

Using tiny increments. A $500 escalation increment is almost insulting in a hot market. If a cash buyer comes in with no contingencies, your extra $500 means nothing. Increment size should reflect market competitiveness, not wishful thinking.

Not requiring proof of competing offers. This is non-negotiable. Always include language that requires the seller to provide documentation of any bona fide offer that triggers your escalation.

Using an escalation clause when you do not need one. If the home has been sitting for 45 days, there are no competing offers, and inventory is high, an escalation clause just signals that you expected competition — it does not create it. In a slow market, submit your strongest offer cleanly and negotiate from there.

Forgetting the appraisal gap risk. If your escalated price ends up above the home’s appraised value, your lender will only finance up to the appraisal number. Know in advance whether you have the cash reserves to bridge that gap, and only cap your clause at a number you can actually close at.

When an Escalation Clause Actually Makes Sense

Not every offer needs one. Here is when it genuinely gives you an edge.

Use an escalation clause when you are confident there will be multiple offers. Your agent will often know this from conversations with the listing agent, so ask directly.

Use it when you are not willing to lose the home but also cannot afford to emotionally over-bid. The clause keeps the decision rational when the situation feels urgent.

Use it in a competitive seller’s market where homes are regularly selling above asking price. In those conditions, a static offer almost always loses to a buyer who has built flexibility into their offer structure.

What Sellers Think About Escalation Clauses (And Why It Matters)

Here is something most buyer-focused articles skip: not every seller loves an escalation clause.

Some sellers prefer the simplicity of a clean highest-and-best scenario where every buyer submits their final number and the seller picks. Why? Because an escalation clause reveals your ceiling, and some sellers will counter at your cap regardless of where competing offers actually landed.

This is rare, but it happens. A good listing agent will protect their client’s interests, and an experienced seller may use your cap as a negotiating floor rather than accepting the clause outcome.

The fix? Talk to your agent about the seller’s situation. Is it a corporate relocation? An estate sale? A family downsizing on a timeline? The more you know about what the seller actually wants — speed, certainty, flexibility on closing date — the better you can pair the escalation clause with other offer terms that make your bid feel complete, not just financially competitive.

The One Question You Need to Answer Before You Write the Clause

Before you submit any offer with an escalation clause, ask yourself one honest question:

If the clause triggers at my maximum cap, can I close this deal — financially, emotionally, and logistically — without regret?

If the answer is yes, the clause is the right tool.

If there is any hesitation, adjust the cap. The purpose of this strategy is not to win at any cost. It is to win within your boundaries, on your terms, with full clarity about what you are agreeing to.

That is exactly what it did for me.

Final Thought

Losing three homes in four months was genuinely demoralizing. But looking back, those losses forced me to get smarter about how competitive real estate offers actually work.

An escalation clause is not a magic trick. It does not guarantee you win. It does not replace a strong pre-approval, a clean offer, or a well-timed submission. But when the market is moving fast and emotions are running high, it brings a structure that keeps you competitive without compromising your budget.

And in my case, it was the difference between watching someone else move into the home I wanted — and handing over the keys myself.

Disclaimer: Real estate laws and escalation clause regulations vary by state and locality. Always consult with a licensed real estate agent and a real estate attorney before including an escalation clause in your purchase offer.