Buying a house feels impossible — until you have a real plan. A down payment that feels like a mountain you’ll never climb. If you’ve ever looked at your bank account and thought “I’ll never afford a home,” You’re not alone.

But here’s the truth: thousands of everyday people on average incomes buy homes every year. Not because they got lucky. Because they built a focused, consistent savings strategy — and stuck to it.

This guide gives you exactly that. 20 proven, practical strategies to save money for a house faster than you thought possible — built for real life in 2026.

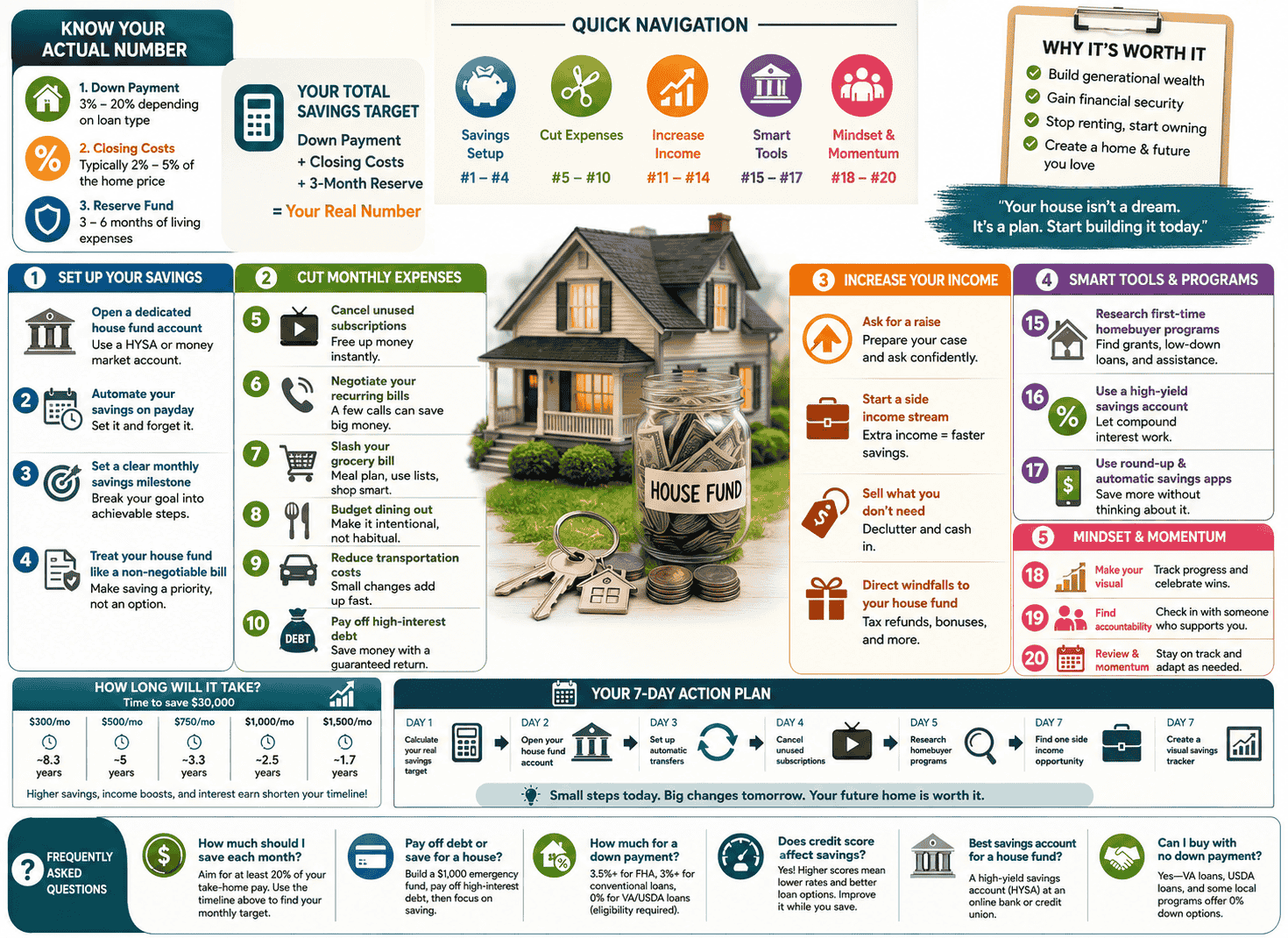

Before You Start: Know Your Actual Number

The single biggest mistake future homebuyers make is saving without a target.

Before you cut a single expense or open a new savings account, you need to know exactly how much you’re saving for. That means understanding:

1. The Down Payment

The down payment is your largest upfront cost. How much you need depends on the loan type you qualify for:

| Loan Type | Minimum Down Payment |

|---|---|

| Conventional Loan | 3% – 20% |

| FHA Loan | 3.5% (with 580+ credit score) |

| VA Loan (military) | 0% |

| USDA Loan (rural areas) | 0% |

Important: Putting down less than 20% on a conventional loan typically means paying Private Mortgage Insurance (PMI) — an extra monthly cost until you build enough equity. Factor this into your long-term plan.

2. Closing Costs

Most first-time buyers forget about closing costs entirely. These typically run 2% to 5% of the home’s purchase price and cover things like appraisal fees, title insurance, lender fees, and legal costs.

On a $300,000 home, that’s $6,000 to $15,000 on top of your down payment.

3. Move-In and Emergency Reserves

Experts recommend keeping 3 to 6 months of living expenses in reserve even after buying. Homes come with unexpected costs — a broken water heater, a roof repair, an HVAC issue — and you don’t want to drain your emergency fund on day one.

Your Total Savings Target Formula:

Down Payment + Closing Costs + 3-Month Reserve = Your Real Number

Write that number down. Put it somewhere visible. Every strategy in this guide works toward hitting it.

Quick Navigation

| Category | Strategies |

|---|---|

| Savings Setup | #1 – #4 |

| Cutting Monthly Expenses | #5 – #10 |

| Increasing Your Income | #11 – #14 |

| Smart Saving Tools | #15 – #17 |

| Mindset & Momentum | #18 – #20 |

Part 1: Set Up Your Savings the Right Way

1. Open a Dedicated House Fund Account — Separate From Everything Else

This is the first and most important step. Open a savings account used exclusively for your house fund. Give it a name like “House Fund 2026” if your bank allows it.

Why it matters: Money sitting in your everyday account gets spent. Money sitting in a separate, named account with a clear purpose gets protected. Out of sight, out of mind — in the best possible way.

Best account types for a house fund:

- High-Yield Savings Account (HYSA) — Earns significantly more interest than a standard savings account. In 2026, many HYSAs offer competitive APYs that meaningfully grow your balance over time.

- Money Market Account — Similar to an HYSA with slightly different features; worth comparing rates.

Avoid putting your house fund in investments like stocks or crypto. You need this money to be stable and accessible — not subject to market swings.

2. Automate Your Savings on Payday

Every financial expert agrees on this: automate your savings before you have a chance to spend the money.

Set up an automatic transfer from your checking account to your house fund account on the same day you get paid. Even if it’s $100 or $200 per paycheck, automation makes it consistent and effortless.

The psychology behind it: When you transfer manually, you make a decision every payday. Sometimes you talk yourself out of it. Automation removes that decision entirely. The money moves before your brain registers it as available.

Start with whatever amount feels sustainable. Increase it by $25 every two to three months.

3. Set a Clear Monthly Savings Milestone

Your overall target number can feel overwhelming. Break it down into monthly milestones that feel achievable.

Example:

- Target: $30,000 (down payment + closing costs + reserve)

- Timeline: 3 years (36 months)

- Monthly savings needed: ~$833/month

Now you have a concrete monthly goal instead of a distant, intimidating number. If $833 feels too high, extend your timeline or find ways to increase your income (more on that below).

Pro tip: Use a simple savings tracker — a spreadsheet, a printable chart, or a savings app — to mark your monthly progress. Seeing the bar move is more motivating than most people expect.

4. Treat Your House Fund Like a Non-Negotiable Bill

Rent is non-negotiable. Your phone bill is non-negotiable, Your electric bill is non-negotiable.

Your house fund contribution should carry the same weight.

When you frame savings as optional, it gets skipped the moment life gets expensive. When you frame it as a fixed obligation — equal to any other bill — it becomes automatic behavior. The mindset shift is small but the impact is enormous.

Part 2: Cut Monthly Expenses and Free Up Cash

5. Audit Every Subscription and Cancel What You Don’t Use

The average household pays for multiple subscriptions they barely use. Streaming services, gym memberships, apps, software, news paywalls, meal kit boxes — they add up quietly.

Do this today:

- Open your bank statement and credit card statement

- Highlight every recurring charge

- Ask honestly: Did I use this in the past 30 days?

- Cancel everything you didn’t use

Cancelled subscriptions free up money immediately — with zero impact on your daily quality of life.

Common ones people forget: Free trials that converted to paid, old cloud storage plans, apps from previous phones, and annual subscriptions buried in your email history.

6. Renegotiate Your Biggest Recurring Bills

Your internet, phone, insurance, and even some utility bills are negotiable — most people just never try.

How to negotiate:

- Call your provider and mention a competitor’s current rate

- Ask specifically for a “retention offer” or “loyalty discount”

- Be politely willing to cancel — this unlocks better deals

A 10-minute phone call can routinely save $20 to $50 per month on internet alone. Applied to phone, car insurance, and other recurring bills, you can easily free up $100 to $200 per month with a few calls.

The math: $150/month saved = $1,800/year straight into your house fund.

7. Slash Your Grocery Bill Without Eating Worse

Food is one of the most controllable expenses in any budget. With a few consistent habits, most households can cut 20 to 30 percent from their grocery spending.

High-impact grocery habits:

- Meal plan every week — Know exactly what you’re cooking before you shop. Buy only what you need.

- Write a list and follow it — No list means impulse purchases every trip.

- Switch to generic brands for staples — flour, rice, pasta, canned goods, cleaning supplies. The quality difference is minimal to nonexistent.

- Shop at discount grocers — Compare prices at Aldi, Lidl, or regional discount stores versus your usual supermarket.

- Reduce food waste — The average household throws away a significant amount of food each month. Use what you buy before it goes bad.

8. Cut Dining Out to a Specific, Budgeted Number

Eating out regularly is one of the fastest ways to drain a savings plan. This doesn’t mean never eating out — it means making it intentional and budgeted rather than a daily default.

Practical approach:

- Set a firm monthly dining-out budget (example: $150/month for a couple)

- Track it in real time so you know where you stand

- Keep restaurant meals as a planned, enjoyable occasion — not a response to not feeling like cooking

If you currently spend $400/month eating out and reduce it to $150, that’s $250/month — $3,000/year going toward your house instead.

9. Reduce Transportation Costs

After housing, transportation is often the second largest expense in a household budget. Small changes here free up significant money.

Ways to reduce transportation spending:

- Carpool to work even two or three days per week

- Consolidate errands into one trip to reduce fuel consumption

- Refinance your car loan if rates have improved since you took it out

- Shop around for car insurance annually — loyalty rarely pays

- Delay the next car upgrade — every year you drive a paid-off vehicle instead of taking on a new payment saves thousands

10. Eliminate or Reduce High-Interest Debt First

This strategy might seem counterintuitive in a savings guide, but it’s critical.

If you’re carrying credit card debt at 20% or higher interest, paying that down aggressively is saving money — at a guaranteed 20% return. No savings account or investment reliably beats paying off high-interest debt.

Recommended approach:

- Build a small emergency fund first ($1,000 minimum) so unexpected expenses don’t go back on credit cards

- Then attack high-interest debt aggressively using either the avalanche method (highest interest first) or the snowball method (smallest balance first)

- Once the debt is cleared, redirect every dollar you were paying toward your house fund

Eliminating a $300/month credit card payment is the same as giving yourself a $300/month raise — all of which can now go toward your home.

Part 3: Increase Your Income to Save Faster

11. Ask for a Raise — With a Prepared Case

The fastest way to increase your monthly savings is to earn more. And the highest-leverage place to start is your current job.

If you haven’t asked for a raise in the past year, prepare your case and ask.

How to build your case:

- Document specific accomplishments with measurable results

- Research market rates for your role (Glassdoor, LinkedIn Salary, Levels.fyi)

- Request a formal meeting with your manager — don’t bring it up casually

- Be specific: ask for a number, not a vague “increase”

A 5–10% raise on a $50,000 salary adds $2,500 to $5,000 per year — all of which can flow directly into your house fund.

12. Start a Side Income Stream

A part-time income source dedicated entirely to your house fund can dramatically compress your timeline.

Side income options by time commitment:

| Low Time (5–10 hrs/week) | Medium Time (10–20 hrs/week) |

|---|---|

| Freelance writing or editing | Tutoring or teaching |

| Selling unused items online | Delivery driving (food or packages) |

| Pet sitting or dog walking | Virtual assistant work |

| Online surveys and tasks | Handmade goods on Etsy |

The key rule: Every dollar earned from your side income goes directly into your house fund — not into your regular spending.

Even $300 to $500/month from a side income adds $3,600 to $6,000 per year to your savings timeline.

13. Sell What You Don’t Need

Walk through your home and identify everything you no longer use — electronics, clothing, furniture, sports equipment, tools, collectibles.

Sell them on Facebook Marketplace, eBay, Depop, or local buy/sell groups. A thorough declutter can generate $500 to $2,000 for most households — a meaningful one-time boost to your house fund.

Bonus: A less cluttered home also clarifies what you actually need in a new home, which helps you avoid buying more space than you need.

14. Direct Every Windfall Straight Into Your House Fund

Tax refunds. Work bonuses. Birthday cash. Inheritance. Freelance payments. Side hustle income.

Every windfall you receive is a house fund opportunity. Most people let windfalls dissolve into lifestyle spending within weeks of receiving them.

Make a rule: Any money you weren’t counting on in your monthly budget goes directly into your house fund — before you have time to think about spending it.

A single $2,000 tax refund deposited immediately saves you roughly 4–6 months of regular contributions.

Part 4: Use Smart Tools and Programs

15. Research First-Time Homebuyer Programs in Your Area

This is one of the most underused strategies available to first-time buyers.

Many federal, state, and local programs offer:

- Down payment assistance grants (money you don’t have to repay)

- Low or zero down payment loans

- Below-market interest rates for qualifying buyers

- Closing cost assistance

Programs vary significantly by location, income level, and home price. Research what’s available in your specific area through:

- Your state’s Housing Finance Agency website

- HUD-approved housing counselors (free service)

- Your local credit union or community bank

Some buyers reduce their required savings by tens of thousands of dollars through programs they didn’t know existed.

16. Use a High-Yield Savings Account and Let Compound Interest Work

Where you keep your house fund matters. A standard savings account at a big bank may earn almost nothing in interest. A high-yield savings account (HYSA) can earn meaningfully more on the exact same money.

Example: $15,000 in a standard account at 0.01% APY earns roughly $1.50/year. The same $15,000 in a HYSA at a competitive rate earns significantly more — effectively free money toward your goal.

Shop for the best current HYSA rates at sites that aggregate and compare rates across banks. Online banks and credit unions typically offer the most competitive options.

17. Use Round-Up and Automatic Savings Apps

Several banking apps and tools automatically round up every purchase to the nearest dollar and transfer the difference to savings. Others analyze your spending patterns and automatically move small amounts you won’t notice into savings.

These micro-savings tools won’t replace deliberate saving, but they add a consistent trickle on top of your main contributions. Over 12 months, many users accumulate an extra $200 to $600 without any conscious effort.

Part 5: Mindset and Momentum

18. Make Your Goal Visual and Impossible to Ignore

Abstract savings goals are easy to deprioritize. Visual goals are harder to ignore.

Create a simple savings thermometer, a progress chart, or a milestone tracker and put it somewhere you see every day — on your refrigerator, your bathroom mirror, or your phone’s lock screen.

Every time you hit a milestone ($5,000, $10,000, $15,000), acknowledge it. Celebrate modestly. Then set your eyes on the next marker.

The psychology: Progress visibility keeps motivation alive during the long middle stretch — the period between excited starting and exciting finishing where most people give up.

19. Find an Accountability Partner or Community

Saving for a house is easier when someone else knows about your goal.

Tell a trusted friend, partner, or family member about your target and your monthly milestone. Check in with them monthly. Even knowing someone will ask “how’s the house fund going?” keeps you more consistent than going it alone.

If you don’t have someone in your immediate circle, online communities focused on personal finance and homebuying are full of people on the same journey.

20. Review and Adjust Your Plan Every 3 Months

Life changes. Income changes. Expenses shift. A savings plan you set in January may need adjusting by April.

Every three months, sit down and review:

- Are you hitting your monthly milestone? If not, why — and what changes?

- Has your income increased? If yes, can you increase your monthly contribution?

- Has a big expense been eliminated? Direct those freed-up dollars to your house fund.

- Is your timeline still realistic? Adjust if needed — without guilt.

A savings plan that gets reviewed and adjusted regularly outperforms a rigid plan that gets abandoned.

How Long Will It Take? A Realistic Timeline

Here’s a realistic look at how long it takes to save $30,000 (a common target for a first home) at different monthly savings rates:

| Monthly Savings | Time to $30,000 |

|---|---|

| $300/month | ~8.3 years |

| $500/month | ~5 years |

| $750/month | ~3.3 years |

| $1,000/month | ~2.5 years |

| $1,500/month | ~1.7 years |

Note: These estimates don’t account for interest earned in a HYSA or windfalls — both of which can meaningfully shorten your timeline.

The takeaway: increasing your monthly savings from $500 to $1,000 cuts your timeline nearly in half. That’s why the income-increasing strategies in this guide matter as much as the expense-cutting ones.

Your House-Saving Action Plan: Start This Week

You don’t need to implement all 20 strategies at once. Here’s a simple first-week action plan:

Day 1: Calculate your real savings target (down payment + closing costs + reserve) Day 2: Open a dedicated high-yield savings account for your house fund Day 3: Set up an automatic monthly transfer on payday Day 4: Audit your subscriptions and cancel unused ones Day 5: Research first-time homebuyer programs in your state or city Day 6: Identify one side income opportunity you could start within 30 days Day 7: Create a visual savings tracker and put it somewhere visible.

Seven days. Seven concrete actions. That’s enough to build real momentum.

Please read this article to learn: How to save money on groceries.

Frequently Asked Questions

How much should I save each month for a house?

It depends on your target and timeline. A common guideline is to save at least 20% of your take-home pay. If homeownership is a priority, direct as much of that 20% as possible toward your house fund. Use the timeline table above to find the monthly number that fits your goal.

Is it better to pay off debt or save for a house?

Both matter, but sequence matters too. Build a small emergency fund first ($1,000). Then aggressively pay off high-interest debt (above 7–8%). Once that’s clear, shift focus to your house fund. Low-interest debt (student loans under 5%) can often be managed alongside saving.

How much do I need for a down payment in 2026?

It varies by loan type. FHA loans allow as little as 3.5% down with a 580+ credit score. Conventional loans start at 3% for some programs. However, putting down 20% eliminates PMI and reduces your monthly payment significantly. Research what loan types you qualify for before deciding on a target.

Does my credit score affect how much I need to save?

Yes, significantly. A higher credit score typically means a lower interest rate, which means lower monthly payments — and you may qualify for better loan programs. If your credit score needs work, improving it while you save for a down payment is time well spent.

What’s the best savings account for a house fund?

A high-yield savings account (HYSA) at an online bank or credit union. Look for the highest current APY with no minimum balance requirements and no monthly fees. Avoid mixing your house fund with any investment account — stability matters more than growth for a short-to-medium term goal.

Can I buy a house with no down payment?

Yes, in some cases. VA loans (for eligible military members and veterans) and USDA loans (for eligible rural areas) offer 0% down payment options. Some state and local programs also offer down payment assistance grants. Research your eligibility before assuming you need a large down payment.

Final Thoughts

Buying a house is one of the biggest financial goals most people will ever work toward. It takes time, discipline, and a plan that holds up in the real world — not just on paper.

But it is absolutely achievable. Not just for high earners. Not just for people with perfect finances. For regular people who decide to take it seriously, build the right habits, and stay consistent month after month.

Start with the number. Build the system. Automate where you can. Find extra income where possible. And keep your eyes on the goal — because the day you hold those keys will make every sacrifice worth it.

Your house isn’t a dream. It’s a plan. Start building it today.

Last updated: 2026 | Estimated reading time: 12 minutes